At What Age Should I Start to Save?

Future-saving is an essential step people should take to prepare for their financial security. It can be challenging to think about saving money when there are numerous immediate expenses. However, saving early and evading common financial mistakes can aid you on your way to a brighter financial future.

The importance of saving early cannot be overstated. Even small amounts of money saved consistently over time will add up in the long run. The earlier and more regularly you save, the more time your savings have to grow, and compound interest will work its magic. Starting early also helps with budgeting better throughout life as it allows us to plan ahead and ensures enough funds are available in case of unexpected expenses or emergencies.

Why Start Saving Early?

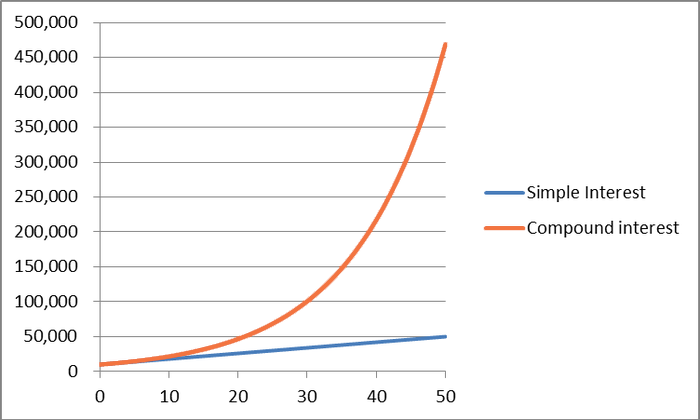

Compound interest

Compound interest is a financial mechanism that can benefit those looking to build long-term wealth and security. It's a powerful force that allows money to grow exponentially over time with minimal effort. Understanding the power of compound interest is the key to making it work for you. Compound interest occurs when an individual or business earns interest on their deposited funds, which are then used as part of the principal amount to generate more earnings. As this process continues, the amount of money grows accelerated due to both principal and previously earned interest being reinvested into future earning opportunities. This type of "compounding" enables larger returns over longer periods than traditional savings accounts or investments alone could achieve.

Credit: teradata.com

Long-term financial goals

Having long-term financial goals is an important part of any personal journey to financial success. Not only can it help you stay motivated and on track, but having a clear roadmap for your future finances can also take the guesswork out of saving and budgeting. When it comes to creating your plan, the first step is deciding what kind of goal you want to work towards. Are you looking for retirement savings? A down payment for a house? Decide what type of goal works best for your individual circumstances and create an actionable plan. Make sure to include milestones along the way so that you can celebrate successes as well as course correct when needed. Your long-term financial plans provide structure while also allowing some flexibility in how you reach them – something that's key if life throws unexpected curveballs along the way.

Best Strategies for Saving

Creating a budget

If you want to manage your finances, having a budget is key. A budget allows you to plan ahead and gives you an idea of what expenses are coming up – this way, you can make sure that you're not overspending or getting into debt. Having a budget doesn't just help with significant expenses like rent and bills – it also helps with smaller purchases like groceries, dining out, entertainment costs, and more. Making a detailed list of all your expected incoming (paychecks) and outgoing funds (bills) will help you organize your spending. This way, when unexpected costs arise (like car repairs), you know exactly where the money is going to come from instead of being caught off guard.

Paying off debt

Getting out of debt can be a tough decision for many people, but it's worth it. Paying off debt not only boosts your credit score, but it gives you more peace of mind too. Whenever you pay off your debt, your credit score will go up because creditors see that you're making on-time payments and trying to reduce your debt. As a result, future loans and credit cards could have lower interest rates, potentially saving you thousands. As a bonus, when debt repayment is less stressful, it's easier to handle other aspects of your life, like relationships and your job. Last but not least, paying off your debt gives you more financial freedom since you won't have any balances to worry about.

Credit: mint.intuit.com

Investing in retirement accounts

Retirement accounts are intended to provide financial security during older age when income may be limited or nonexistent. When investing in retirement accounts, contributions create immediate tax deductions, lowering taxable income and reducing the amount owed at the end of the year. Additionally, when placed in an account earmarked for retirement purposes, earnings accumulate without being taxed until they are withdrawn from the account. Compound interest also increases earnings potential over time because it's calculated on both principal amounts and any accrued interest.

Automating savings

Automating savings is an important tool for individuals to utilize to save money. Automating savings is setting up automatic transfers from your primary checking account into a designated savings account. This saving allows individuals to grow their savings without needing to make deposits actively. Automating savings has various benefits, including helping you consistently save money and reach financial goals faster. It keeps track of all your transactions, so you know exactly how much money you put away each month. Additionally, automating your savings can help eliminate the temptation of spending extra money instead of saving it - because the money is already in a separate account before it even has a chance to enter into circulation.

Saving Strategies for Any Age Groups

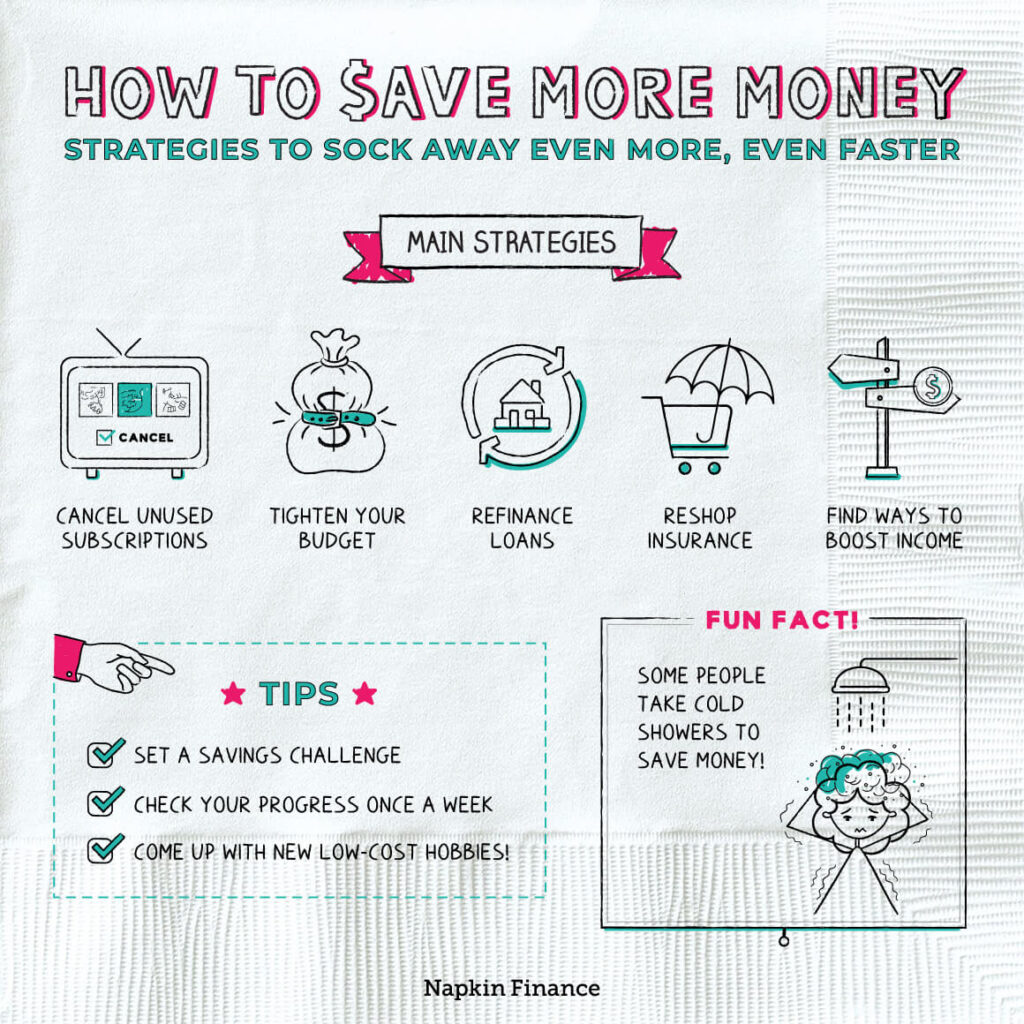

Start with a budget: Putting together a realistic budget based on your income and expenses will help you determine where to cut expenses. For instance, instead of buying lunch every day, pack it. Alternatively, you could downsize your living situation to lower rent.

Automate savings: Invest or save money automatically from your checking account. You can save 600 this way without even thinking about it by setting up an automatic 50 transfer each month.

Avoid debt: In order to avoid unnecessary interest charges, avoid getting into debt as much as possible. The average American household is in debt of $167,463. The most common type of debt is credit card debt, followed by mortgages and car loans.

Live below your mean: Keep your expenses low by living frugally and avoiding unnecessary costs. You could use public transportation or ride-sharing services instead of buying a car to save money. According to the BLS survey, the most significant expenditures for Americans were housing and transportation, which comprised 26 percent and 13 percent of people's take-home pay, respectively.

Consider a side hustle: Make extra income by taking on a part-time job or freelancing. This can help you save more and reach your financial goals faster. The average side hustle earns $686 per month, according to a survey of 1,006 respondents.

Use credit wisely: Keep your credit card balances down and pay them off every month to avoid paying high-interest charges. The average credit card APR is currently just over 16%, which means any interest rate below that threshold can be considered "good."

Invest for the long term: Invest in a retirement account or other long-term investment vehicles to take advantage of compound interest. According to retirement planners, 401(k) portfolios usually generate an average annual return of 5% to 8%.

Credit: napkinfinance.com

To sum up

It is never too early to start thinking about saving money. Taking the time to create a savings plan now can help you stay on track and reach your financial goals throughout your life. Early saving equips you with the ability to deal with unexpected expenses or take advantage of opportunities that come up down the road, such as buying a house or investing in stocks.

Now more than ever, it is essential for everyone to be responsible when it comes to their finances. Beginning an early savings program gives you the power to build financial security and stability over time. Developing habits like budgeting, tracking spending and setting aside funds will lay an important foundation for future success and ultimately provide peace of mind.

Creating a plan that works best for you should be done in small steps so that it can become part of your daily routine without being overwhelming or stressful.