Discover the Standards Banks Use to Approve Personal Loans

Are you considering taking out a personal loan? This article will help explain what banks look at to approve a personal loan.

When applying for a personal loan, it's crucial to understand the criteria lenders consider before approving or denying your application. Banks will evaluate many different factors, such as your income, credit score, debt-to-income ratio, and more when deciding if they are willing to grant you a loan.

It's also important that potential borrowers understand how their credit history and current financial situation impact their eligibility for obtaining a personal loan. Doing your research can help you feel more confident in the decision-making process of whether or not to apply for one.

Read on to find out what banks look at when evaluating an applicant's eligibility for a personal loan!

1. Credit Score

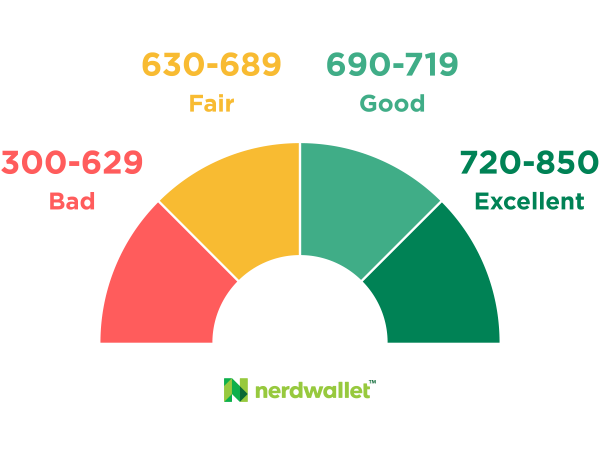

A credit score is a numerical value used by banks and other lenders to measure an individual's creditworthiness. It is usually between 300-850. The higher the number, the better your credit score. A good credit score increases one's chances of getting loan approval. In contrast, a low credit score may result in a rejection or a higher interest rate.

When applying for any type of loan, particularly a personal loan, lenders will review an individual's credit history and associated scores to determine their trustworthiness as a borrower.

Credit scores are determined by examining factors such as payment history, the amount owed on accounts, types of accounts held, and the length of time these accounts have been open.

Generally, most lenders are looking for borrowers with a score of at least 650 to approve them for a loan. A higher credit score usually means lower interest rates on your loan and more favorable terms over the long run. Depending on the lender, someone with an excellent score of 760 or above may get access to better deals than someone whose credit rating is slightly above average.

Lenders also look at how often an individual applies for new loans or lines of credit to gauge the risk level associated with providing them funds.

Credit: nerdwallet.com

2. Income

Monthly income plays a significant role in determining whether or not an individual will be approved for a personal loan. Naturally, higher incomes tend to make individuals more desirable borrowers due to their better ability to repay the loan on time. Banks also consider other financial information, such as tax documents and bank statements, when evaluating someone's loan application.

3. Debt-to-Income ratio

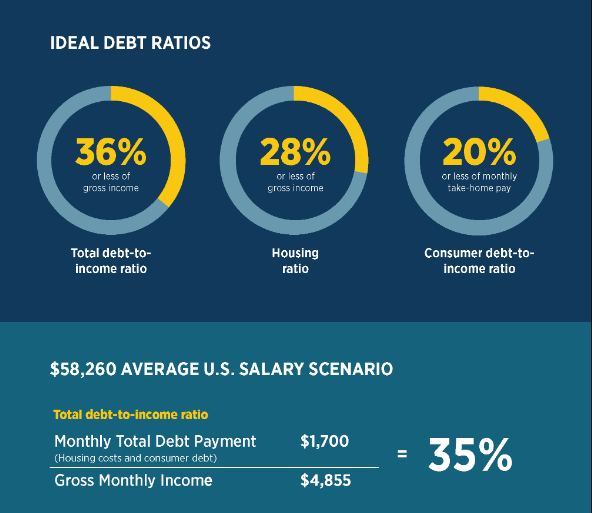

The debt-to-income ratio (DTI) is a proportion that reflects how much of your income goes toward paying off debts. It can help lenders assess an individual's ability to manage their finances and make payments on time. Banks typically look at both front-end and back-end ratios when considering loans, so it's vital to understand what each entails. Front-end DTI involves only housing costs, such as mortgage payments or rent. At the same time, the back end includes all debts, including student loans, car payments, credit cards, and other obligations.

The lower this number is, the more favorable it looks to potential lenders because it suggests you are not financially overextended already and have enough money left over each month for other expenses.

The ideal debt-to-income ratio should be 43% or lower; however, different lenders will have their own requirements for the ratio, ranging from 30 - 50%.

Credit: usaa.com

4. Collateral

Collateral is an asset or property that can be used to secure a loan. When applying for a personal loan, lenders often require borrowers to pledge collateral as security against the loan amount. Collateral helps protect the lender if the borrower defaults on loan repayment.

Collateral gives lenders more assurance that they will receive repayment of any loaned funds. Borrowers who do not have personal assets or credit history may struggle to qualify for a personal loan without providing collateral, making it an important factor in determining whether someone is eligible for a loan.

Assets such as real estate, vehicles, and securities are common forms of collateral used by lenders in approving loans. In addition, banks sometimes accept borrowers' cash deposits as collateral for securing loans.

The two most common types of personal loans with collateral requirements are secured or home equity loans and car title loans. Secured or home equity loans use your property as collateral and usually have lower interest rates than unsecured personal loans. Car title loans use the vehicle you own as security against the loan and typically have higher interest rates because they are short-term solutions for emergency cash needs.

Before signing any loan agreement, it's important to be aware of all terms and conditions, including whether or not the lender requires collateral for the loan.

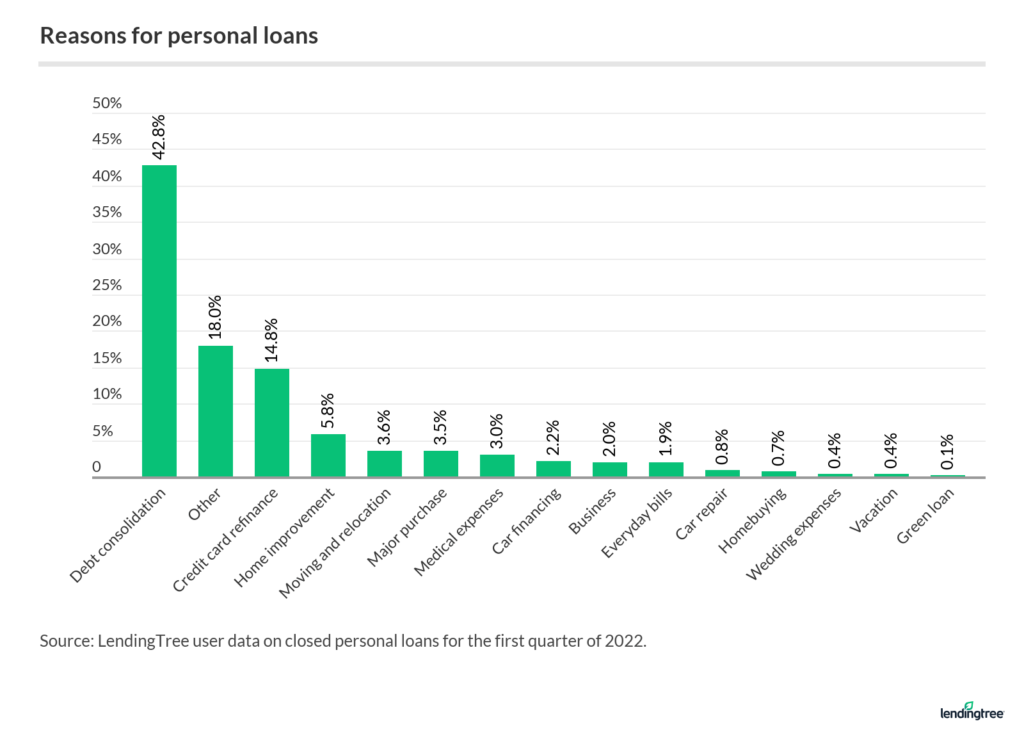

5. The purpose of the loan

When a borrower applies for a personal loan, banks are increasingly interested in not just the credit rating but also the purpose of the loan. Without knowing what the money is being used for, it isn't easy to decide whether or not to approve the loan. Understanding why someone wants to borrow money can give insight into their financial situation and help determine if they are likely to be able to repay their loan on time.

The purpose of the loan can tell lenders how high-risk a borrower might be. For example, applicants who need money for medical bills or emergency expenses may be more likely to repay their loans than those intending to use it for vacation or luxury items like jewelry and electronics.

6. Employment

Employment indicates an individual's ability to repay the loan and provide financial stability. Without reliable proof of employment, banks cannot assess an applicant's creditworthiness. Banks rely on verified income statements to determine if a person can afford their monthly payments.

If an applicant does not have steady employment, banks may require them to list assets that will cover the loan repayment cost in case they cannot make payments on their own. Banks also look at other forms of collateral, such as real estate or investments, when assessing whether or not an applicant should receive a personal loan.

What is the most common reason a bank will deny a loan request?

When applying for a personal loan, it can be disheartening when banks deny your request. But what are the most common reasons that banks reject applications?

The first reason is insufficient income. Banks must assess whether you have enough money to cover the monthly payments on the loan and still leave enough left over to cover living costs. If your debt-to-income ratio is too high or you don't meet their minimum income requirements, they may not approve your loan request.

Another reason for rejection could be having a bad credit score or a history of late payments. Lenders consider this as an indication that you might not pay back the loan in full, so they may decide it's too risky to lend you money.

Credit: lendingtree.com

What is the personal loan approval process?

The personal loan approval process typically involves several steps:

Application: The borrower fills out a loan application using an online, in-person, or phone application. Personal and financial information like employment history, income, and credit score will be requested.

Processing: Once the application is received, the lender will analyze it and check the borrower's credit score. Borrowers' income and employment status will also be verified. For debt-to-income calculations, lenders review the borrower's assets and liabilities.

Underwriting: The lender will determine approval or denial of the loan after reviewing the borrower's information. Upon approval, the lender will determine the interest rate and loan terms.

Approval or Denial: Details about the loan terms, such as interest rate, repayment schedule, and fees, will be provided to the borrower by the lender.

Funding: Borrower funds will be disbursed if the loan is approved. Lenders can transfer funds directly to borrowers' bank accounts or send checks.

Repayment: Paying the loan as agreed is the borrower's responsibility, starting with the first scheduled repayment. Lenders may take legal action if borrowers default on their loans.

To sum up

When applying for a personal loan, there are specific steps you can take to increase the odds of getting approved. Being prepared and knowledgeable about the personal loan approval process is key to being accepted for a loan.

Before you embark on the application process, reviewing your credit history and score is important. Lenders will consider this when assessing your eligibility for a loan; having an excellent credit rating will go a long way in securing approval. Additionally, providing proof of adequate income and meeting other requirements like age verification or collateral may be necessary to receive financing.

Once you've readied all your documents, ensure the information provided on your application is accurate before submitting it. Any discrepancies could lead to delays or rejection.