Exposing the Hidden Dangers of Personal Loans

You can use personal loans for things like home repairs, medical bills, or consolidating credit card debt, but you should be aware of the risks before you take out a loan.

We'll look at the risks of personal loans in greater detail in this article so you know if a personal loan is right for you. The effects of high interest rates, loan defaulting, losing collateral, and overspending will be discussed. We talk about other possible risks and how it's essential to consider everything before taking out a personal loan.

1. Risk of Losing Collateral

The risk of losing collateral is a very real consequence of taking out a personal loan. When an individual takes out a loan, they are essentially putting up some type of collateral as security for the lender to ensure the loan amount will be repaid in full. However, if one fails to keep up with their payment schedule, there is always the possibility of losing this collateral.

The most common types of collateral for personal loans are vehicles and homes. In cases where vehicle loans have been defaulted on, lenders may repossess them and resell them at auction to recoup the loan recipient's money. Similarly, home mortgages can result in foreclosure if the borrower does not keep up with payments. This can lead to severe financial hardship as any equity built prior will be lost too.

2. High Interest Rates

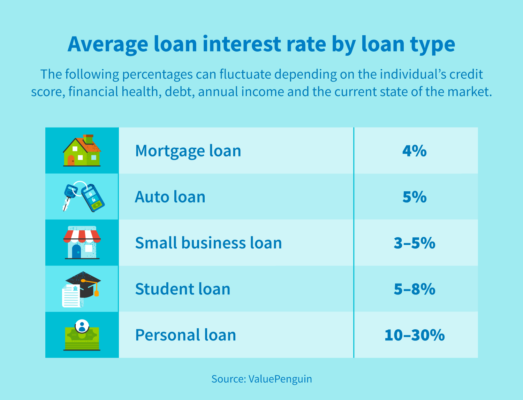

With high interest rates, the potential risks of taking out a personal loan can be significant. When considering taking out a personal loan, it's vital to be aware of the various terms and conditions that come with it, including the interest rate. A higher interest rate can mean an increased risk of defaulting on payments or finding yourself in debt for more extended periods than initially anticipated.

Apart from making repayment more expensive, high-interest rates also reduce your ability to qualify for a loan in the first place. If you have poor credit or limited income, lenders may not approve your application, or they might only offer you loans with high interest rates.

This means that you may end up paying much more than expected on such loans as lenders use these higher rates to offset their perceived risk when lending money to people with questionable credit histories.

Credit: creditrepair.com

3. Temptation to Overspend

One significant risk associated with personal loans is the temptation to overspend. With guaranteed money from the loan provider, people may feel they can use the extra funds on anything they want without consequence.

Unfortunately, this could lead borrowers into further debt and potentially cause them difficulty repaying their loan in full. Many people get into a vicious cycle of borrowing more money to pay off their previous debts. Setting and sticking to a budget can help you avoid this.

To avoid this issue, borrowers should take time to consider what they need the loan for and ensure they are only spending within their means.

4. Difficulty in paying back the loan due to unexpected life events

When taking out a personal loan, one of the risks you are signing up for is the potential difficulty in paying back the loan due to unexpected life events. Unexpected life events can range from sudden job loss to expensive medical bills or even a divorce. These types of issues can make it difficult for borrowers to repay their loans in a timely manner.

Nevertheless, borrowers can take some steps to minimize their risk of defaulting on a loan due to unexpected life events. One way is to plan ahead and be mindful of how much debt they're taking on, depending on their current financial situation. Borrowers should also research different lenders and choose one who has flexible repayment options in case they face any changes down the line.

5. Potential reduction in your credit score if you miss payments

When planning and considering the potential risks of a personal loan, understanding how missing payments could affect your credit score is crucial.

A reduction in your credit score can be detrimental to your ability to access other financial products and services and potentially increase the cost of those products or services.

A lower credit score due to missed payments on a personal loan can also have wider ramifications, such as not being able to secure employment or rent an apartment, insurance being more costly, or even bank accounts being closed.

Therefore, taking steps towards mitigating the risk of missing payments should always be top of mind for all borrowers. Proactively budgeting, setting up payment reminders, and using automated repayment methods are just some ways to ensure that you don't fall behind on your repayments.

Credit: mybanktracker.com

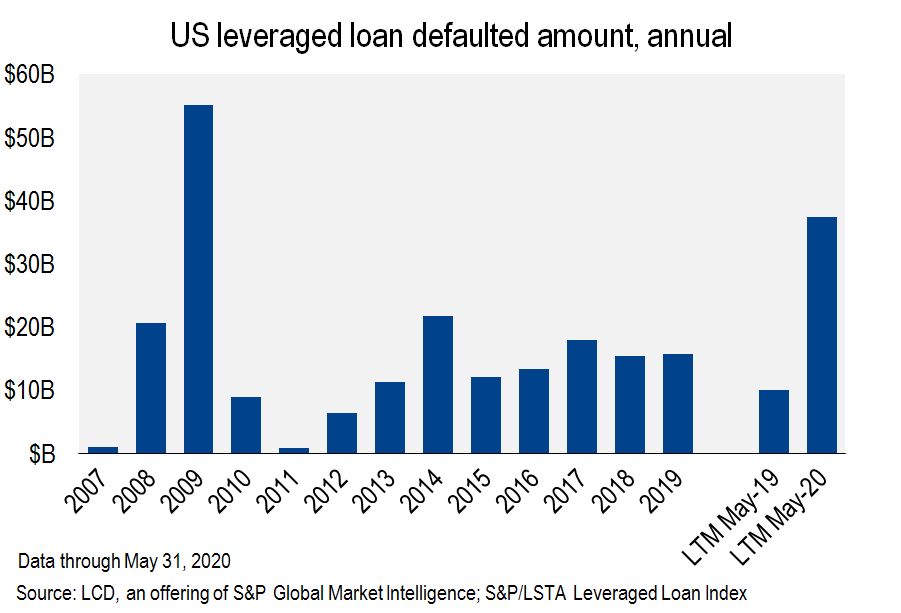

6. Potential for Default

Defaulting on a personal loan means the borrower has failed to make payments as agreed with the lender, which could have serious legal or financial repercussions. Defaulting can have long-term impacts on creditworthiness, making it difficult for the borrower to take out loans in the future when needed.

Before taking out a personal loan, borrowers must understand what default means and how it affects them. Investopedia explains that default occurs when payments are more than 90 days late.

A missed payment can result in late fees or higher interest rates and damage one's credit score. Multiple missed payments can lead to being sued by the lender or having assets seized by creditors.

7. Risk of getting into a debt cycle, taking out new loans to pay off existing loans

A debt cycle occurs when an individual has difficulty making payments on their existing loan(s) and must take out additional loans to pay for those debts. Doing so can have serious consequences, leading to further financial difficulties due to the compounding interest from multiple loans. Moreover, such cycles can become unsustainable if payments are not made in a timely manner or if borrowers cannot make sufficient payments due to insufficient income.

It's important to remember that getting into debt can be easy but extremely hard to get out of without credit counselors or financial professionals' help.

Credit: spglobal.com

8. Stress caused by loan payments and worries about repayment

Financial stress can significantly burden many people, especially when managing personal loan payments. Before committing to a personal loan, understanding the potential risk associated with it is vital. Not only do you need to consider the amount of money borrowed, but also how much you will be required to pay back each month and over what time.

It is easy to overlook the financial strain caused by monthly loan payments in pursuit of achieving a desired goal or purchasing something that had previously been unaffordable. Although beneficial in certain circumstances, if not appropriately managed, personal loans can quickly become overwhelming and cause additional worry about being able to repay them on time and without any extra charges or fees.

To sum up

In conclusion, taking out a personal loan is not without risks. Whether financing a purchase or consolidating debt, you must be aware of the potential pitfalls you may face. From rising interest rates to unexpected fees and penalties, the above list of personal loan risks should give you an idea of what to look for when taking on this type of loan. Ultimately, it's important to do your due diligence and research all available options before committing to a personal loan.