Hidden Risks of Personal Loans

Regarding personal loans, it's easy to get caught up in the excitement of having extra cash to use for whatever you need. Whether it's consolidating credit card debt, paying off medical bills, or taking a much-needed vacation, having access to quick cash can be tempting. However, as someone who has taken out a personal loan, I've learned some severe disadvantages to consider before making a decision.

High Interest Rates

The most obvious downside of taking out a personal loan is that you will pay more interest due to their high rates. Interest rates on personal loans are typically much higher than those found on mortgages and car loans, making them an expensive way to access funds. Additionally, the rate could be even higher if your credit score isn't great when you apply for a personal loan. Therefore prospective borrowers must understand this risk upfront before applying for a personal loan with high interest rates.

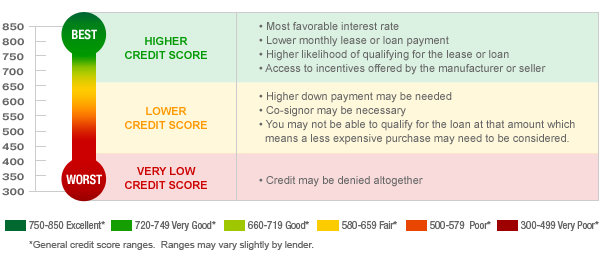

Credit Score Impact

There is a potential for detrimental effects on an individual's credit score to be significant and long-lasting. After taking out a personal loan, you may have difficulty qualifying for future loans or credit cards.

Lenders look closely at your debt-to-income (DTI) ratio when you take out a personal loan. This indicates how much debt you have relative to your income—the higher the number, the greater risk of defaulting on a loan. Additionally, taking out multiple loans further increases this ratio, causing your credit score to drop significantly. Also, if you miss payments or make them late on any type of loan or credit card payment, it will hurt your overall credit rating and raise your DTI ratio even more.

Credit: loanry.com

Risk of Default

Defaulting on a personal loan is one of the many potential disadvantages of which borrowers should be aware before taking out a loan. Default occurs when a borrower fails to make payments as required by the lender's terms and conditions.

When this happens, lenders are allowed to charge borrowers late fees and penalties and even report it to credit bureaus which can cause severe damage to their credit score. This could also impact their ability to take out future loans and increase their overall cost of borrowing due to higher interest rates or additional fees associated with bad credit history.

Therefore, before signing agreements, borrowers must understand the risks of obtaining a personal loan. It is also recommended that they have an emergency fund in place to avoid defaulting in case they cannot make payments on time.

Short-term Solution

When you have financial difficulties, personal loans may only solve them for a short time, but they won't fix the situation for a long time. You may be tempted to get a personal loan, especially if you have an unexpected expense or an emergency. But you have to remember this type of loan isn't the most suitable option for addressing long-term financial difficulties.

Several potential disadvantages are associated with taking out a personal loan, such as high interest rates and fees. Additionally, relying on these loans could lead to further debt down the line as they are often used for consumer spending rather than covering essential costs. Furthermore, these loans don't address the root causes of your financial trouble – such as mismanaging your budget or having too much debt already - which will only resurface once you've paid off the loan.

Additional Fees

One of the key drawbacks associated with personal loans is that they often come with additional fees and charges beyond just interest payments. These can include origination fees, prepayment penalties, and late payment fees that can add up quickly and significantly increase the overall cost of the loan.

Origination fees are one-time charges which are usually a percentage of the total amount borrowed. They may also be referred to as application or processing fees and typically range from 1-6%, based on your credit rating. Additionally, some lenders may charge you a penalty for paying off your loan early, so make sure to read all terms carefully before signing any agreement.

Credit: forbes.com

Potential for Misuse

Personal loans can be a great tool to consolidate debt, cover unexpected expenses, and finance large purchases. However, they also come with potential risks when misused. Misuse of personal loans can lead to financial problems if not managed carefully.

When taking out a loan, it is important to consider the potential for misuse and the associated disadvantages. Without proper management and planning, it is easy to overspend on unnecessary or frivolous items that do not align with your long-term financial goals. This kind of spending can place a strain on your finances by increasing monthly payments and overall debt load – resulting in difficulties making payments or paying off the loan entirely.

To avoid misusing a personal loan, it's critical to understand how much you need and develop a budget plan that allows you to set aside money for repayment each month.

Limited Flexibility

When it comes to loan terms and repayment options, personal loans often have shorter terms than other loan types and require regular payments with interest over those shorter periods. These tight timelines may make it difficult for borrowers who experience cash flow issues or need more time to repay their debts. Unlike other types of loans, there are usually no deferment options available, and late payments may result in additional fees or even additional interest charges. In addition, many lenders impose penalties for early repayment of a personal loan balance which can significantly reduce the financial benefit of making extra payments toward your debt.

To sum up

Personal loans may seem like an easy solution to financial problems, but they come with some serious disadvantages that should be considered before making a decision. High interest rates, limited flexibility, negative impact on credit scores, and the potential for misusage are all necessary elements to consider.

It's important to weigh the pros and cons and make sure you can afford the loan and the monthly payments before taking the plunge. And think twice before using the loan for unnecessary or frivolous expenses.

Be informed, take into consideration your financial situation, and ensure a personal loan is the right choice for you. You shouldn't use a personal loan to make your situation worse.