How Do I Determine Dow Much Personal Loan I Can Afford to Borrow

Prior to taking out a personal loan, you should specify how much you are able to reasonably afford. Knowing precisely how much you can borrow and still be able to make timely payments will help guide your decisions and set realistic expectations. Furthermore, understanding the total cost of the loan, including interest rates, fees, other charges, and repayment terms, is vital when weighing any type of personal loan.

Budgeting for expected expenses throughout the loan is a critical factor in determining how much personal loan you can afford. Before applying for a personal loan, consider all your current debts and financial obligations, such as rent/mortgage payments, car loans, or credit cards that must be paid each month in addition to any additional costs you may have incurred due to changes in your life such as job loss or medical bills.

Factors to Consider

The decision to apply for a personal loan is important, and it's essential to understand how much you can afford. Various factors should be reviewed before determining the amount of personal loan you can borrow.

Firstly, your current financial situation, including your income and expenses, must be considered. Your loan amount should not exceed what you make monthly; otherwise, repaying your loan will become problematic. Additionally, look into any existing debt obligations like credit card payments or other loans before deciding the amount of personal loan that fits your budget.

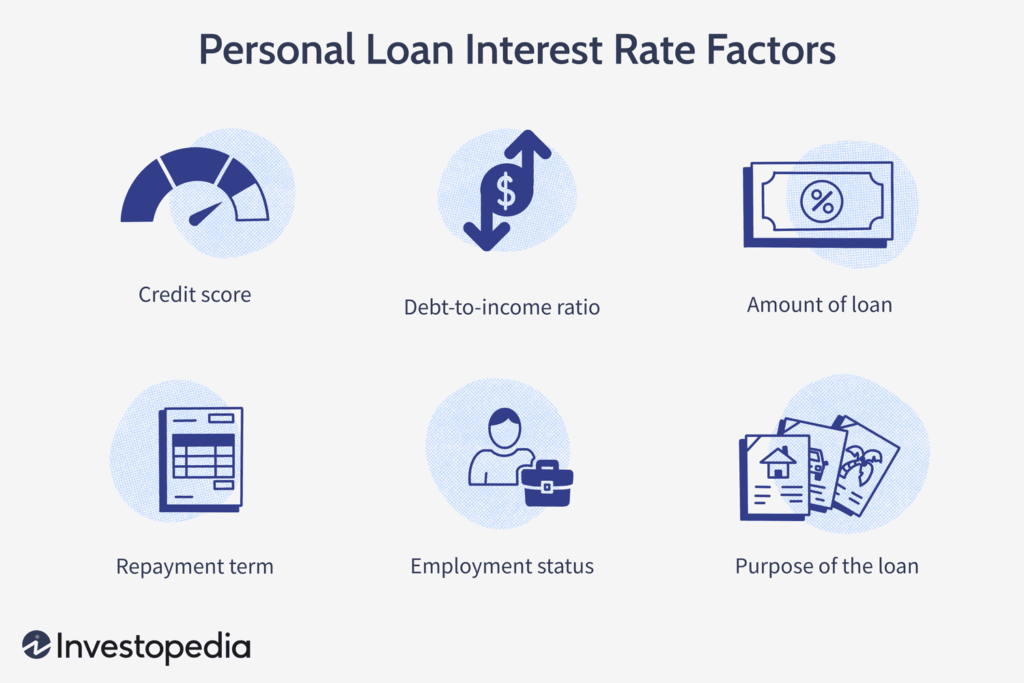

Another factor to remember is the type of interest rate attached to the proposed personal loan - whether fixed or variable – as this will influence overall costs over time and may affect repayment options later.

When applying for a personal loan, you should consider your income, expenses, credit score, and debt-to-income ratio. Knowing how these four factors affect the amount of money you can borrow will help you determine the best loan option.

Your income plays a key role in the amount you can borrow; lenders will use this figure to assess whether or not they can offer you a loan. Generally, lenders prefer if your income is consistent over time so that they know that you are likely to be able to repay them on time. Expenses also need to be considered when assessing how much money someone can afford to borrow.

Credit: investopedia.com

Affordability Calculators

Affordability calculators can be an excellent tool for those looking to take out a personal loan. They allow potential borrowers to estimate how much they can afford to borrow based on their current financial situation. Understanding the impact of taking out a loan is an important step in guaranteeing that you are not over-extending yourself financially, and affordability calculators are a great way to start this process.

These tools ask questions about your income, expenses, and other debts. From this information, they can calculate how much additional debt is feasible based on your current financial circumstances. This provides valuable information when deciding whether or not borrowing money is right for you at this time, as well as understanding the affordable amount given your budget and lifestyle.

Modern technology provides an array of helpful calculators for individuals seeking to manage their finances better. From loan payment calculators to debt-to-income ratio calculators, numerous options are available for those wishing to calculate how much they can afford when taking out a personal loan. Budgeting calculators provide a comprehensive look into your finances, allowing you to make informed decisions about your spending habits.

These calculators are handy and enable you to efficiently work out the details of a personal loan and assess its affordability. The information collected through these tools helps you determine the best course of action regarding any financial decision–saving money on monthly bills or setting up a budget plan that works with your income.

Determining a Reasonable Monthly Payment

Many consumers find themselves unsure of how much they should borrow and how much their monthly payments should be. Knowing the right amount for your monthly payment can help you avoid overspending and any potential financial distress later on. Here is an explanation of how to determine a reasonable monthly payment for a personal loan.

Creating an accurate budget takes some work and planning, but with clear information on how much you can afford, it becomes easier to stick to it. Begin by assessing your current income and fixed expenses like rent, mortgage, utility bills, phone bills, and insurance premiums. Subtract these from your total income to get an idea of what remains for discretionary spending or saving. If needed, consider adjusting fixed expenses by cutting back on unnecessary costs or increasing revenue with a 2nd job or side hustle.

Credit: lendingtree.com

To sum up

Taking out a personal loan can be an attractive way to finance a large purchase or consolidate existing debt, but it's important to consider carefully the amount of money you can realistically commit to repaying. Knowing your budget and understanding the potential implications of taking on too much debt are key to making informed decisions about personal loans.

Before applying for a personal loan:

Take time to determine how much money you're comfortable borrowing and how long you may need to repay it.

Consider your current financial situation as well as any unexpected costs that could arise during repayment.

Research different lenders and their terms, such as interest rates, fees, prepayment penalties, and repayment periods.