Personal Loans: Dire Consequences For Defaulting

Defaulting on a personal loan is a decision that should never be taken lightly. It's a serious matter with far-reaching consequences that can devastate your financial stability and overall well-being.

The ripple effects of defaulting on a personal loan can be felt for years to come, leading to irreversible damage to your credit score, legal action, additional fees and interest charges, difficulties in meeting other financial obligations, emotional stress, and even impacts on personal relationships.

This article will detail the potential consequences of defaulting on a personal loan and demonstrate how a momentary loss of judgment can lead to a lifetime of regret.

1. Damage to credit score

Defaulting on a personal loan can significantly impact an individual's credit score, making it difficult to obtain future loans or credit. When someone defaults on a loan, they essentially break their promise to make the agreed-upon payments. This results in negative marks being placed on the borrower's credit report, significantly lowering their score and thereby making future financing more difficult.

Not only will this person likely be unable to borrow from traditional banks or lenders, but they may also find that other forms of credit, such as store cards and mobile phone contracts, become off limits too. A default on a personal loan can have devastating consequences. The default could prevent individuals from accessing financial assistance for years, potentially hindering their ability to purchase big-ticket items such as cars or property.

2. Additional fees and interest charges

Understanding the terms of a personal loan is a critical step before signing anything. This includes being aware of the interest rates and fees associated with defaulting on payments. For example, many lenders charge late fees when payments are not received by the due date. Additionally, interest rates may increase, leading to more money being repaid over time than originally borrowed.

Plan your repayment strategy for any personal loan you take out by keeping these fees and penalties in mind. This way, you won't get into financial trouble and pile up debt.

3. Difficulty meeting other financial obligations

Defaulting on a personal loan isn't something to be taken lightly. Not only will it affect an individual's credit score, making it harder for them to access credit in the future, but defaulting on a personal loan can also make it difficult for an individual to meet other financial obligations.

A significant consequence of defaulting on a personal loan is that an individual may find themselves unable to keep up with loan payments on other forms of debt, such as mortgages or car loans. This could lead to repossession or foreclosure due to non-payment and worsen matters. Additionally, depending on the severity of the situation, they may even face legal action from creditors seeking repayment of the original loan plus any additional associated fees or interest rates.

Credit: lendingtree.com

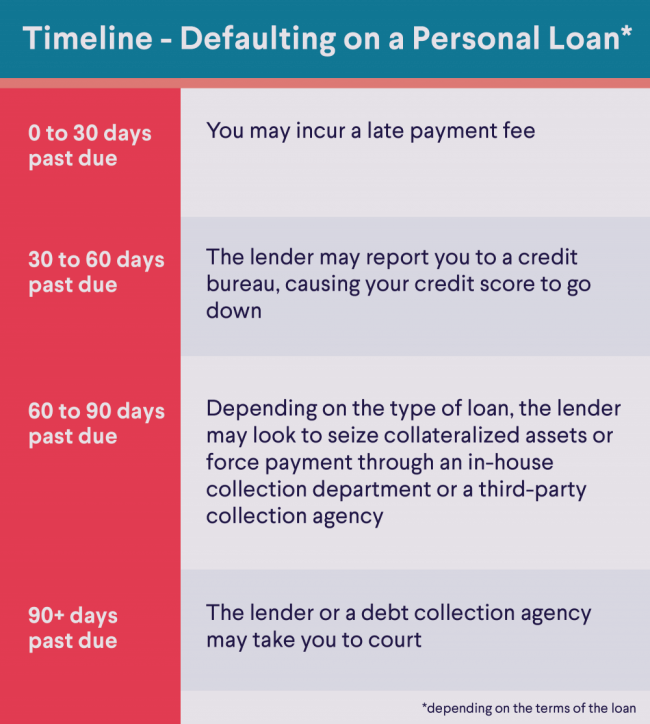

4. Legal action

Lenders can take legal action against those who fail to pay back their debts as per the loan agreement. These actions may include filing lawsuits, garnishing wages, or freezing bank accounts. In extreme cases, lenders may even press charges against borrowers for failing to repay the loan. Thus, borrowers need to understand the repercussions before taking out a loan and ensure that they can honor any commitments made while taking out the loan to avoid any legal action from lenders.

5. Legal Fees

If a borrower fails to make regular payments or misses payments altogether after agreeing to a personal loan, it may result in the creditor taking legal action.

This could mean that the borrower incurs high legal fees from the defense costs to challenge any claims made by the creditor. Alternatively, if found liable, the debtor may be required to pay further fees as part of any reparation order issued by the court.

It is important to note, however, that not all creditors will take legal action against defaulting borrowers and instead may attempt to negotiate repayment plans out of court. In some cases, this might avoid paying costly legal fees and result in reduced interest rates or forgiveness of specific amounts owed.

6. Judgment against the borrower

Attaching assets means the lender has the legal authority to take the items offered as collateral or security to pay off the loan balance. This could include anything from real estate properties and motor vehicles to jewelry and other valuables.

When defaulting on a personal loan, borrowers should know what measures their lender takes when collecting funds. In most cases, lenders will attempt various collection activities before taking more serious steps, such as attaching assets. This includes attempting to negotiate payment arrangements with borrowers or referring them for debt counseling services.

7. Emotional stress

Defaulting on a personal loan can be a difficult and stressful situation, both financially and emotionally. It is important to understand that the emotional stress associated with defaulting on a personal loan can seriously affect one's mental health. The feeling of overwhelming guilt and shame can cause increased stress, depression, and anxiety.

Being in debt is never ideal, but it especially becomes problematic when it involves a personal loan because it may involve a breach of trust between the borrower and the lender. This breach of trust can lead to feelings of betrayal and worthlessness accompanied by bouts of sadness or depression. Additionally, fear or embarrassment could be associated with explaining the situation to family members or friends.

These emotions must be addressed along with any financial issues arising from defaulting on the loan.

Credit: sofi.com

8. Impact on personal relationships

Deciding not to repay a loan can be damaging to those who cosigned or are financially responsible for that loan. For instance, if a family member or friend cosigned on a loan and the borrower defaulted, they would be liable for the remaining balance.

It is important to recognize the impact that defaulting has not only on your credit score but also on any relationship tied to that particular loan. The lender will likely seek repayment from whoever is legally responsible for the debt - regardless of their relationship with you.

This could lead to strain between both parties as they struggle with repayment plans or dispute financial responsibility.

It is recommended that families and friends consider all other options before entering into an agreement where one person cosigns another's debt.

To sum up

It's important to remember that defaulting on a personal loan should always be avoided if possible. If you're experiencing financial difficulties, it's essential to seek help and explore alternatives before defaulting on a loan.

It may be difficult, but being honest with yourself and your lender about your financial situation is crucial. Many lenders have hardship programs and options for customers who are struggling to make payments. It's always worth looking into those before defaulting.

In short, defaulting on a personal loan should be considered as a last resort, not only because of the immediate financial consequences but because of the long-term effects that can be felt for years to come. It's crucial to always be thoughtful and careful before making such a critical decision.