Retirement: Discover the Best Ways to Save!

Have you been worrying about getting your retirement savings in order? Don't worry. You're not alone! Read on to learn more about the best ways to save for retirement and put your mind at ease.

Here are some quick tips:

Create a retirement budget: Establish a budget for your retirement savings and expenses.

Start early: The sooner you start saving, the more money you'll have when you retire.

Maximize your employer match: Contribute enough to take full advantage of any employer match.

Diversify your investments: Consider a mix of stocks, bonds, and other types of investments.

Set up automatic deposits: Automatically transfer money from your paycheck or bank account into a retirement account.

Stay informed: Monitor your investments regularly and make adjustments as needed.

Planning for retirement should be part of everyone's overall financial planning goals. Although there are many ways to save for retirement, it is essential to understand the different types of savings plans and how they work for you.

Retirement savings plans provide you with various investment options and other features, such as tax advantages, employer contributions incentives, and eligibility and distribution rules.

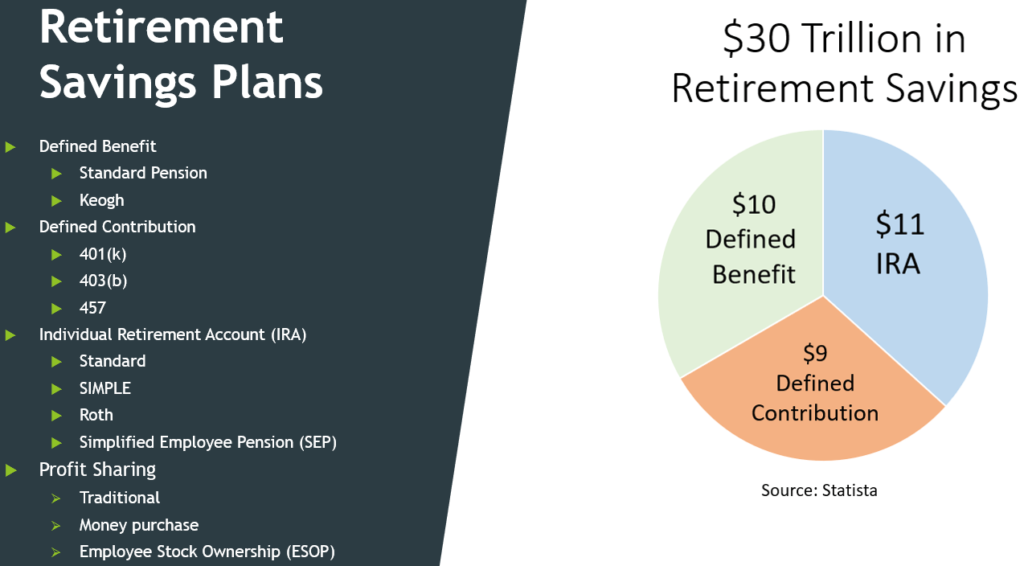

These types of plans include traditional Individual Retirement Accounts (IRA), Roth IRAs, employer-sponsored retirement savings plans like 401(k)s, and Simplified Employee Pension (SEP) IRAs.

It is also important to understand state programs such as 529 college savings plans that give you an additional option when investing in your future.

Setting up a realistic budget that enables you to save regularly is another way to ensure that your retirement dollars are working hard for you.

Last but not least, individuals need to consider the impact of Social Security benefits on their total retirement income plan.

Understanding the various components of your plan will position you well when decisions need to be made on how best to invest in your future.

The Benefits of Saving for Retirement

Saving for retirement may seem time-consuming and complex, but doing so has many potential benefits. Setting aside money for your future allows you to build a more secure financial life with fewer worries when you retire. Here are the most important benefits of saving for retirement:

Saving money now will support your lifestyle in later years. Most retirees require some form of financial support during their golden years, whether from Social Security or other sources. By saving early on in life, you create a nest egg that can cover some or all of those expenses.

You can reduce your tax burden by contributing to an IRA: Making contributions to an Individual Retirement Account (IRA) may reduce your taxable income.

Take advantage of employer-matched contribution programs: Many employers will match employee contributions towards a Retirement Savings Plan up to certain maximum limits. This means that if you invest money in your account through paycheck deductions, depending on the amount and other factors, your employer might also put an equivalent amount in.

Save earlier rather than later: It’s never too late to start saving for retirement — but it pays off if you get started sooner rather than later! Compound interest over time will increase even small amounts saved regularly into sizable.

Make use of investment vehicles such as annuities and trusts: An annuity is an investment option that allows individuals to put away enough money now that they receive payments in the future at regular intervals (e.g., monthly). Trusts are another way people can hedge against inflation while creating storehouses of wealth they could draw from when needed during retirement years.

Credit: seekingalpha.com

Types of Retirement Savings Accounts

When you are ready to start planning for retirement, there are a few types of accounts that can help you reach your goals. Investing in the correct type of retirement account can be the key to successful long-term savings. Here is an overview of several different types of accounts which could be used for retirement savings:

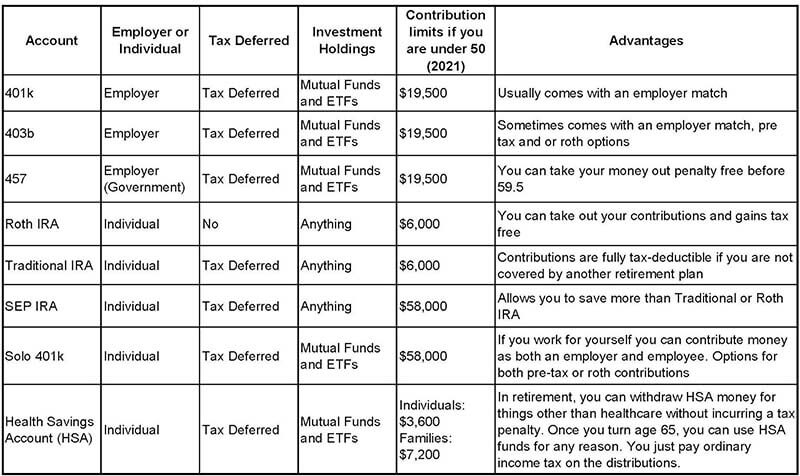

Individual Retirement Accounts (IRA) – An Individual Retirement Account allows you to save up to $6,000 per year, depending on your individual situation. This type of account is tax-free and offers several investment options, including stocks, bonds, and mutual funds.

401(k) – A 401(k) is a tax-advantaged retirement plan offered by some employers that allow employees to save pre-tax money and build up a nest egg for the future. Employees typically contribute part of their paycheck before taxes each month, and employers may offer matching contribution amounts too.

Roth IRA – A Roth IRA requires after-tax contributions but offers tax-free growth potential on all future earnings, such as interest or dividends. The money you earn in a Roth IRA will not be taxed when it's time to withdraw them during retirement as long as certain conditions are met.

Annuities – An annuity is an insurance product designed for long-term capital accumulation and income protection during retirement by making regular payments over an extended period. Annuities provide secure income throughout your retirement years with no stock market risk but have been known to have hidden fees or charges attached, which should be considered before investing in one.

It's important to remember that all of these plans have different rules, so it's essential to do your research before deciding which method best fits your needs and desired outcomes when saving for retirement.

Credit: baylaart.com

Strategies for Saving for Retirement

Saving for retirement can be daunting. You’re likely too young to truly appreciate how the decisions you make today will affect your future success, and you may find it difficult to think about a time in the distant future when you won’t be able to work due to age or health reasons.

With that said, a few strategies and tips can help make saving for retirement easier while also helping keep your financial goals in line.

The first step is to create a realistic and achievable plan. Aspirational goals are great, but at some point setting achievable tasks is far more beneficial. This includes deciding when you would like to retire, how much money you will need saved up for that time, and then breaking down year-by-year savings goals for the lead-up to that period.

Contributing to individual retirement accounts (IRA): Backing these contributions with pre-tax funds helps maximize savings potential while decreasing federal tax liabilities associated with those funds over time. Additionally, many employers offer matching grants on these accounts, which can result in an even greater return on investment.

Investing in stocks, bonds, certificates of deposit (CDs), mutual funds, and annuities: This provides returns and hedging against inflation over long periods, which may also be beneficial for achieving retirement goals. The stock market allows investors access to immediate liquidity should funds be needed. But with this method, it’s crucial to maintain close monitoring and strict risk limits.

An emergency fund is vital for planning unexpected expenses or lifestyle changes. Investing safely and prudently as part of a financial planning strategy is also a good idea. Additionally, contributing to healthcare plans every year can be helpful during retirement.

Professional Financial Advice

Getting advice from a professional financial advisor can be crucial in creating a successful retirement plan. Financial advisors can provide personalized recommendations and tailored advice depending on the investor's needs.

When crafting a retirement plan, professional financial advisors can help by considering your age, income, savings goals, risk tolerance, and investment objectives.

Investing in the stock market can also be complicated, so having a knowledgeable professional assists in making wise investing decisions. In addition to selecting and managing particular investment accounts, advisors can provide valuable information on tax strategies that may help reduce taxes during retirement. They can also help balance investments for increased wealth growth opportunities and preserve capital for retirement income needs.

Financial planners are valuable resources for understanding Social Security options and other government benefits you might qualify for when you begin your retirement journey.

Advisors are trained to help individuals understand different strategies available, such as whether to take Social Security earlier or delay until full retirement age or later. Furthermore, they can clearly explain other available sources of income (such as pensions).

An experienced advisor can give you peace of mind knowing that you have chosen the best path to achieve your goals for a comfortable retirement.

Conclusion

Ultimately, it’s crucial to choose a strategy for saving for retirement that works for you. Different aspects of your financial situation (income, current and future obligations, potential risk tolerance) can influence what kind of retirement savings to choose.

Taking a holistic approach to retirement savings and including both stock investments, annuities, 401(k) plans, and even government pensions can be the best way to ensure a secure financial future in retirement.

Investing in stocks carries more risk than investing in other vehicles, such as certificates of deposit (CDs), but the potential returns may be much higher.

Increasing contributions to tax-advantaged accounts such as 401(k) plan help build wealth without being subject to taxation until the money is withdrawn at age 65 or older. Annuities provide income security, can help supplement other forms of retirement savings, and create stability during volatile markets and times when stock prices go down. Government pensions can provide additional security depending on where you live or have worked.

Saving for retirement takes discipline and dedication. There are many options for individuals looking to invest in their future. Explore each one carefully before making decisions, so you know what’s best for you!