Unsecured vs. Secured Loans

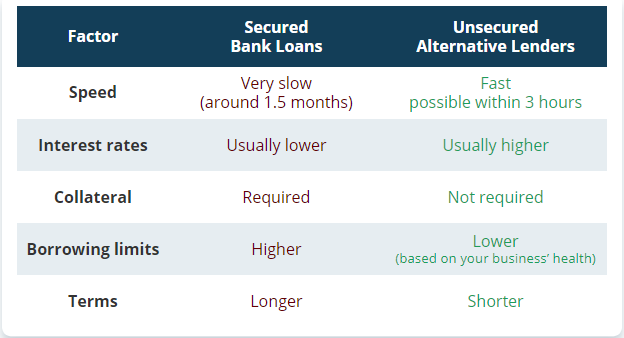

Personal loans can be secured or unsecured. A secured personal loan requires some form of collateral (such as a home or car) that the lender can use in case of default. These types of loans generally have lower interest rates because an asset backs the loan and mitigates some lender risk. Unlike secured loans, unsecured loans don't require collateral. It, therefore, has higher interest rates as there is no asset backing to mitigate risk for the lender.

Whether you choose a secured or unsecured loan, ensure how much interest you’re likely to pay back over time on top of your borrowed base amount. Read through your contract details carefully before signing any agreement with a lender. Make sure that all terms are flexible enough so that repayment doesn’t become overwhelming.

What is a Secured Personal Loan?

A valuable asset, such as a house, car, or other assets, back a secured personal loan. Your collateral is used as security for a secured personal loan if you default on repayment.

Since this type of loan is less risky, interest rates are usually lower. Besides, you may get more money than you would from an unsecured loan. Please remember, however, that if you default on your loan payments and cannot repay your debt, your assets could be seized by your lender according to the terms and conditions of your loan agreement.

Therefore you must consider all options before applying for a secured personal loan. Make sure you research potential lenders thoroughly and determine whether they will provide competitive rates to have the best chance of paying back what you owe on time without penalty fees or additional costs associated with extended payment timeframes.

Features of Secured Loans:

The interest rate is usually lower than with unsecured loans making them more affordable for borrowers.

These loans are easier to obtain because of the collateral provided.

The borrower can negotiate with their lender on how long they have until repayment.

The lender has less risk since they’re able to retrieve the collateral should they need to.

Other fees may be associated, such as appraisal or closing costs.

These are typically used for larger financial items such as cars or homes.

Credit: become.co

What is an Unsecured Personal Loan?

A personal loan that is unsecured does not require you to commit collateral (such as a car or house) when applying. Instead, lenders assemble these loans based on your creditworthiness and income. Unsecured personal loans have many uses, including funding major purchases, consolidating debt, and paying bills. When looking for an unsecured personal loan, borrowers typically have access to fixed-rate loans, meaning their interest rate stays the same throughout the repayment period.

Features of Unsecured Loans:

They don't require collateral and therefore are often quicker to process and easier to apply for than secure options.

The interest rate is higher because lenders assume more risk when approving this type of loan.

Unsecured personal loans can be used for any purpose, like consolidating debts, paying medical bills, financing home improvements, etc.

Credit score plays an important role in whether you'll qualify or not.

These are typically smaller financial amounts used for emergencies.

To sum up

While secured loans have the benefit of offering favorable terms and lower interest rates, there is an element of risk associated with them. If you default on the loan, your lender is legally entitled to reclaim the asset used as security for the loan. On the other hand, unsecured personal loans are relatively easier to obtain and hold less risk since you don't have to put any assets on the line.

Ultimately, secured and unsecured loans can be a good way to obtain extra funds for large purchases or debt consolidation. Before deciding which type best suits your needs, you should carefully review all terms and conditions in your chosen loan agreement to understand what to expect over the life of your loan contract.