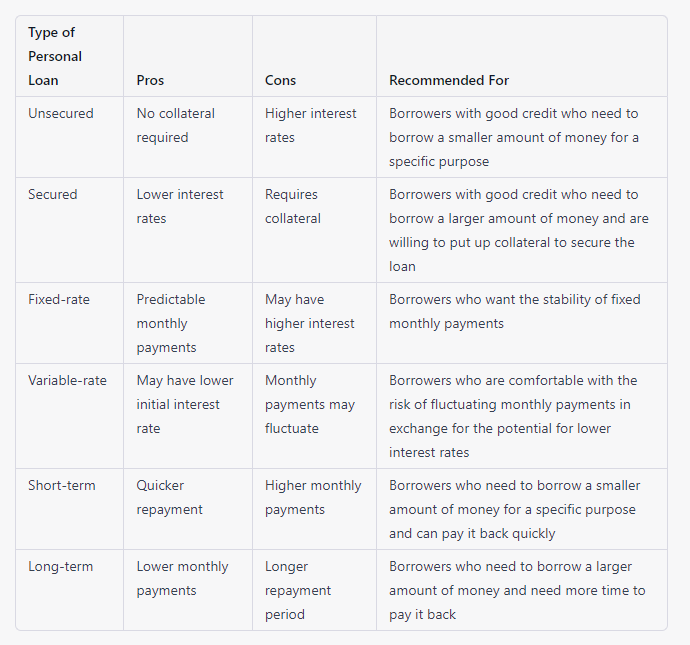

What Types of Personal Loans Are Available?

Personal loans can be used to finance a variety of life projects – from home renovation to starting a business. But if you're considering taking out a personal loan, you must know the various types available. This guide will explore the different kinds of personal loans and how to find the right one for you!

So let's get started – break down the different types of personal loans and see which one fits your situation best.

1. Unsecured personal loans

Unsecured personal loans are a type of loan where the borrower does not have to provide collateral as a security for the lender. This type of loan is purely based on the creditworthiness and trustworthiness of the borrower.

With unsecured personal loans, there is no demand for any security from the consumer. Thus, it is more attractive to many people with no property or asset to put up as collateral.

Unsecured personal loans can be used for many different purposes, such as financing a car, consolidating debt, paying off medical bills, making home improvements, or undertaking a particular project.

A major advantage of an unsecured loan is that it usually allows you to borrow money without having to pledge your house or other assets as collateral.

However, there may also be some drawbacks associated with this type of loan. Generally, higher interest rates and shorter terms will be related to an unsecured loan compared with secured loans since they often present more risk to lenders who do not possess any assurance that their investment can be recovered in case of default by the borrower.

Additionally, people with bad credit will likely have a harder time qualifying for an unsecured loan as lenders require having a good credit score or proof of income/assets, which act as indications for them about your ability to pay back the loan amount in full and on time.

2. Secured personal loans

A secured loan, sometimes called a "homeowner's loan," is a personal loan secured by collateral, usually in the form of real estate, such as a house.

In other words, the borrower puts up their property as security for the loan, and should they fail to meet their payment terms, the bank can repossess and resell it to recoup their losses.

Secured loans will generally offer lower interest rates than unsecured loans since there is less risk for the lender that they won't get paid back.

Secured loans may be used for any purpose, from consolidating debt to home improvements and major purchases such as cars or boats.

However, because there are pros and cons associated with all lending products, it's important to consider them carefully before taking on this type of responsibility.

The primary benefit of secured personal loans is that they provide borrowers with access to significantly more significant amounts of capital than would typically be available through unsecured private financings products such as credit cards or consumer finance companies.

Because securing a loan mitigates risk on behalf of the lender, this will also result in lower interest rates making it easier for borrowers to make financial progress without having an unmanageable monthly payment burden.

Another advantage is that these types of loans offer greater repayment flexibility than most other forms of financing, so borrowers can achieve greater control over their cash flow management when using this type of product.

Additionally, these loans are easily fixed and released from security once outstanding debts have been cleared, which can help make them relatively low cost over time when compared against other forms of borrowing thanks to mortgage exit fees being avoided.

Credit: forbes.com

3. Fixed-rate personal loans

A fixed-rate personal loan is an agreement between the lender and the borrower in which the interest rate on the loan remains constant over its life. In other words, a fixed-rate loan does not change or fluctuate over its term.

Fixed-rate loans offer stability, providing borrowers with consistent payments and predictable interest costs. Additionally, these types of loans have the potential to help individuals better manage their finances.

However, they have different pros and cons that individuals should consider before taking out a personal loan with a fixed rate.

The biggest benefit of a fixed-rate loan is its predictability in terms of financial budgeting. Since you know exactly how much your monthly payments will be, it's easy to plan for them and adjust your budget accordingly, so there are no surprises down the line. This may be an appealing option if you cannot keep up with changing markets or interest rate fluctuations.

Furthermore, since a fixed-rate loan's payment schedule won't change during its term, you remain protected from market swings caused by inflation or recessionary trends.

Despite these benefits, borrowers can miss out on potential savings opportunities if market rates drop during the life of their loan. However, some lenders may offer this option at additional costs.

4. Short-term personal loans

Short-term personal loans are unsecured credit that can help cover the cost of surprise or unexpected expenses such as medical bills. Still, they can also fund vacations, home repairs, tuition payments, and more.

They typically range under $10,000 and can be repaid in one lump sum or in installments over time. Generally speaking, borrowers should expect to receive their money within 1-7 days.

Short-term installment loans are typically easier to qualify for than longer-term ones because they have fewer eligibility requirements. In addition, they offer more flexibility in repayment options and less hassle.

Despite these benefits, short-term personal loans have several significant drawbacks, including higher-than-average interest rates, high origination fees, and short repayment terms. As a result, borrowers need to understand the costs of these loans before taking them out and make sure repayment is possible within the allotted time frame before signing up.

Credit: forbes.com

5. Long-term personal loans

Long-term personal loans are a form of credit available for borrowers to acquire considerable sums of money in one lump sum. The repayment schedule is stretched over an extended period, ranging from a few years to a couple of decades, based on the loan's terms and conditions.

The definition may sound attractive since you will be granted more time to pay back your debt and spread the costs over time.

The pros associated with long-term personal loans include the following:

Lower monthly payments.

More financial flexibility.

No pre-payment penalties.

Fixed interest rates.

Funding for home improvement projects, wedding expenses, and other large purchases.

The cons associated with long-term personal loans include the following:

Over the life of the loan, the interest costs are higher.

More risk from potential rate increases (with variable rate loan options).

Stricter criteria for borrowing eligibility.

Some lenders require collateral such as real estate or other assets.

When considering a long-term loan, you must weigh all the pros and cons involved to determine if your financial situation allows you to repay the amount borrowed during the extended checkout period.

You must also look at multiple lenders before settling on a specific lender or loan product to get an idea about the different offerings available within these products and decide which one works best for you.

6. Variable-rate personal loans

Variable-rate personal loans are a type of loan with an interest rate that can fluctuate depending on the state of the economy. Those looking to finance home improvements, consolidate debt, pay medical bills, or cover unexpected expenses often use this loan.

Unlike fixed-rate loans, which have a constant interest rate for the duration of the loan, variable-rate loans feature an interest rate that is subject to change over time.

Interest rates fluctuate depending on market conditions, and your monthly payments may also increase or decrease.

It's important to remember that while a variable-rate loan may save you money in some situations by giving you access to cheaper financing options at times when rates are lower than usual, it can also work against you if rates start rising and leave you with higher payments than expected.

To sum up

Personal loans can provide an excellent option for those seeking financial aid in times of need. Whether one is looking for an extra source of income, to consolidate debt, or to finance a big purchase, personal loans offer the convenience and flexibility many borrowers are looking for. Depending on the borrower's needs, they can come with both fixed and variable interest rates. Before securing a loan, it is crucial to consider all options and that borrowers choose the best payment plan and loan terms suited to their individual situation.