Which Loans Are Most Easily Approved?

The most accessible loan to get approved depends on your financial circumstances, including your credit score, income, debt-to-income ratio, and employment status. Generally, secured loans are easier to qualify for because the lender has collateral as protection in case the borrower defaults on the loan. Credit unions may also be more likely to approve loans for their members, and some online lenders may have more lenient lending criteria than traditional banks.

Factors that affect loan approval

Your credit score

The credit score is influential in the approval process when applying for a personal loan. Lenders use this number to measure your reliability as a borrower, and it’s essential to understand how it affects your loan application.

The credit score is calculated based on information from your credit report. It includes payment history, the amount owed, and the length of credit history.

Generally speaking, lenders prefer borrowers with higher credit scores since these are seen as more responsible borrowers who make payments on time and reduce their debts.

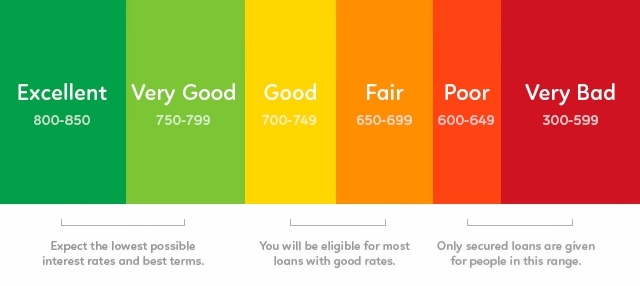

A good credit score for personal loans is typically considered to be 660 or higher. Anything below that may result in either rejection or high-interest rates due to the added risk assumed by the lender.

Higher scores will result in lower interest rates, allowing the borrower access to better terms and conditions on their loan.

Credit: nitrocollege.com

Your income

When applying for a personal loan, lenders use income as one of the most important factors in determining your eligibility.

Your income is used to calculate your debt-to-income ratio, which helps lenders decide if you have enough money to pay back the loan and maintain your current standard of living.

Generally speaking, lenders prefer to approve borrowers with higher incomes because they are seen as having more financial stability and resources to pay off their loans.

Additionally, your income determines how much money you can borrow when applying for a personal loan. Lenders usually set an upper limit on how much they are willing to lend based on the applicant's income. To simply put, the more income you earn, the more money you can borrow.

Your debt-to-income ratio

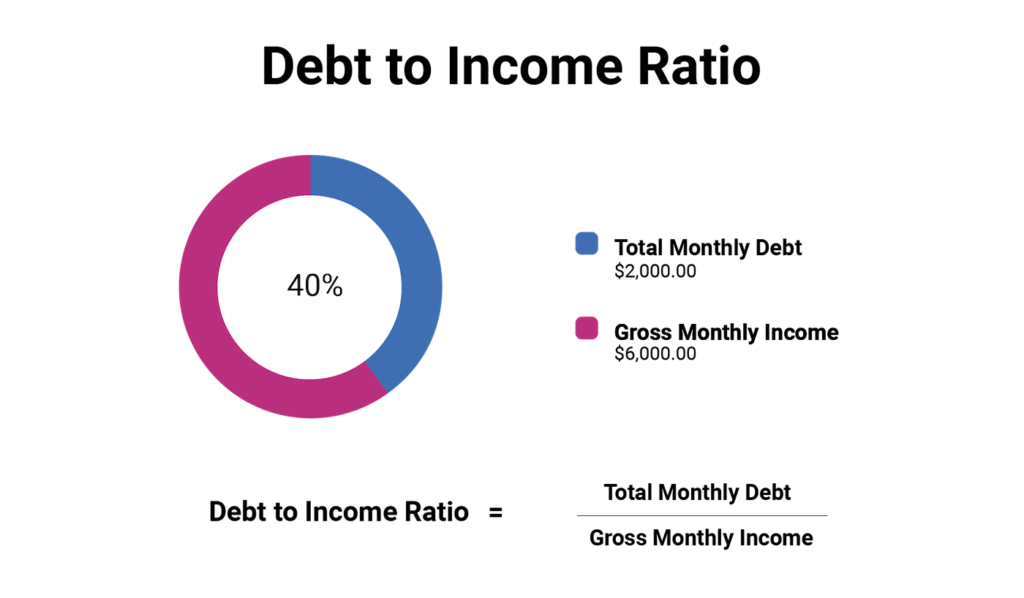

When it comes to personal loans, understanding the debt-to-income (DTI) ratio is a crucial component when trying to get approved. The DTI ratio is a calculation of all your debts compared to your income. To determine this ratio, lenders analyze how much of an individual's gross monthly income goes toward paying off credit cards, student loans, and other debts.

Having a high DTI can be an obstacle to loan approval as it indicates someone may not have enough money left over each month after making payments on their existing debt obligations. A good debt-to-income ratio should be below 36% – this means that no more than 36% of an individual's gross income should be going towards paying off their debts.

Credit: experian.com

Your employment status

Employment status is critical in determining an individual's eligibility for personal loans. Banks and other lenders often rely heavily on employment status to gauge the risk associated with approving a loan. When considering an individual's application, lenders assess whether the applicant has sufficient income to support monthly loan payments.

In most cases, full-time employment is seen as a reliable source of income and, therefore, positively influences personal loan application approvals.

In contrast, those with part-time or freelance jobs tend to have more difficulty obtaining personal loans due to their generally lower incomes and inconsistent job security.

The most preferred category is that of salaried individuals who have an ongoing relationship with their employer and receive regular paychecks every month. The main advantage for such applicants is that they enjoy greater flexibility regarding loan terms and repayment options because their steady income can be used as evidence of creditworthiness.

Self-employed individuals may also qualify, but they must prove steady income over time and provide additional documentation such as tax returns or bank statements.

How to increase the chances of loan approval

Securing a loan can be a daunting task. Due to the variety of options and the unpredictable nature of loan approvals, it is important to understand how you can increase your chances of being approved for a loan.

The first step in increasing your chances of loan approval is having a good credit score or credit report. This will help demonstrate to lenders that you have experience making payments on time and responsible financial habits. Additionally, having documents such as tax returns, pay stubs, bank statements, and other types of evidence showing financial stability will help present yourself in the best light possible when applying for a loan.

Another way to increase your chances of loan approval is by providing information about the purpose of the loan and how you plan on paying back the money borrowed.

Types of loans that may be easier to get approved for

Secured loans

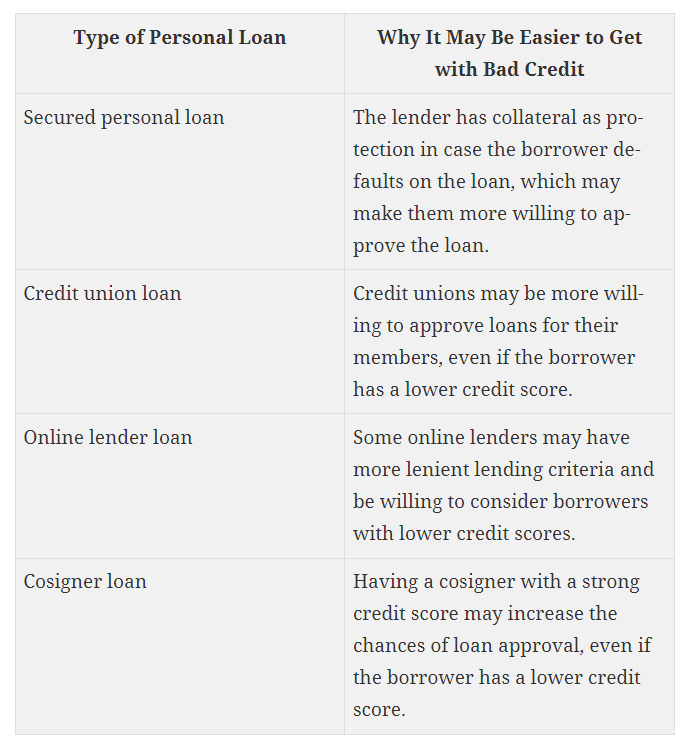

Secured loans are generally easier to approve than unsecured loans, as they require collateral from the borrower to obtain approval. This means that should the borrower default on their payments. The lender would have the right to take possession of the collateral and recuperate their losses.

This type of loan is beneficial for both lenders and borrowers alike. Lenders can offer more competitive interest rates with better terms due to less risk associated with secured loans. At the same time, borrowers benefit by having access to more significant amounts of credit than an unsecured loan would provide.

Loans from a credit union

Credit unions are financial institutions owned and run by its members, typically employees or members of a particular industry. It offers the same services as any other traditional banking institution, including savings and loan accounts, but provides its members with more favorable terms regarding interest rates.

Personal loans from credit unions are more accessible than banks because they focus on building relationships with their members instead of focusing solely on the bottom line.

Credit Unions have fewer stringent requirements for approval and often offer lower interest rates than banks due to their non-profit status.

They also provide access to personalized customer service, which can help you understand how best to use your loan funds and develop an effective repayment plan.

Loans from online lenders

Online lenders are companies that provide personal loans over the internet. These organizations specialize in providing financial services to individuals and businesses who cannot access traditional banking options. Online lenders offer competitive rates and flexible terms for borrowers, making them an attractive option when looking for a loan.

Loans from online lenders are often easier to approve than those offered by traditional banks because of their streamlined application process. They typically require less paperwork and can process applications quickly with minimal hassle.

Plus, online lenders focus on alternative methods of evaluating creditworthiness, such as income, employment history, and current bills paid on time, rather than relying solely on credit scores. This makes it more likely that applicants will be approved even if they have bad credit or minimal credit history.

Cosigner loan

A cosigner loan is a type of loan that requires someone else, the cosigner, to guarantee the repayment of the debt. The cosigner takes on the responsibility for repayment if the borrower defaults on the loan. This makes it possible for borrowers with less-than-perfect credit or limited income to get approved for loans they wouldn't otherwise qualify for.

Cosigners provide assurance to lenders by taking on some of the risk associated with extending credit. Since they are legally obligated to make payments if necessary, lenders feel more secure in approving loans and can often offer better terms and interest rates than what would be available without a cosigner.

In most cases, having a qualified cosigner can make getting approved much easier and faster than waiting months or even years to improve your own credit score and financial history.

To sum up

Remember to take into consideration your credit score, debt-to-income ratio, and the type of loan you are applying for when considering which type of loan is easiest to get approved for. A secured loan tends to have lower requirements than unsecured personal loans due to the collateral backing them. Additionally, government programs such as FHA loans may provide better rates and easier qualifications.