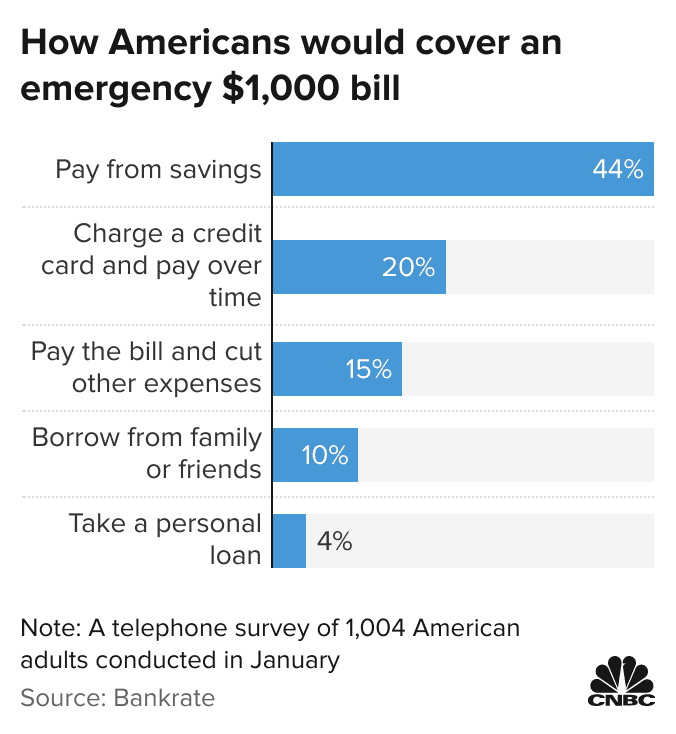

Why being prepared for financial emergencies is crucial

If you're unprepared for financial crises, learning proper management techniques is crucial. These emergencies can occur unexpectedly and wreak havoc on finances, causing stress and anxiety. This informative article stresses the importance of preparing for financial emergencies and equipping readers with the necessary skills to navigate them effectively.

Unexpected expenses: Financial emergencies can come in many forms

There are a variety of financial crises that may arise, causing anxiety and worry for individuals and families alike. The solution to effectively managing unexpected expenses, such as medical bills, car repairs or unemployment, is planning. To ensure one's financial security during unforeseen circumstances, it is crucial to be financially prepared.

Taking the time now will make things easier later. It's important to review your budget and create a plan to save in case of an emergency. Even creating a savings account with money that is transferred every month or setting money aside every time you get paid will give you something to fall back on should anything come up. Finding ways to reduce expenses by cutting back on wants or unnecessary spending can also be beneficial.

Additionally, having the right insurance policies can provide coverage if an unanticipated event arises, such as medical costs or job loss leading to income loss. Doing research in advance to review what coverage works best for your specific industry and needs is critical too. Finally, think about having an emergency fund readily available with at least 3 months of living expenses saved up as another source of security in case of financial difficulty.

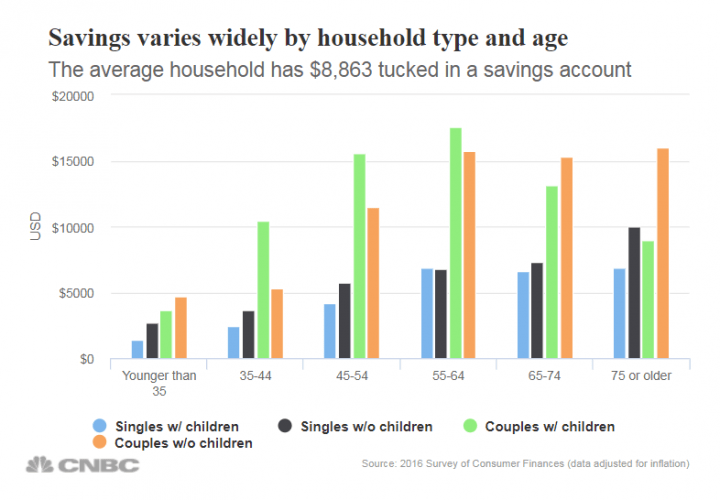

Emergency fund

Maintaining an emergency fund can serve as a reliable approach to securing one's financial standing during unforeseen situations. Essentially, an emergency fund is a designated pool of funds reserved solely for unforeseeable expenses. With an emergency fund in place, it's comforting to know that there is a reliable sum of money available to mitigate any unexpected financial challenges.

Regarding how much to put away, some experts advise covering living expenses for at least three months, while others recommend enough funds to cover six months or more. This will depend on your personal situation, such as your job type and whether it is steady income or freelance work that may have sporadic payments. Once you have determined your monthly living expenses, multiply that amount by the number of months you would like coverage for, and there you will have your target goal for how much to save in an emergency fund.

It's recommended that this money be kept in something like a high-yield savings account or another type of liquid asset such as a CD or money market account so that it is easily accessible when needed without penalty fees or loss on principal amounts invested. Additionally, adjusting spending habits and taking other steps toward reducing debt may help manage costs during difficult times as one prepares for future financial emergencies. Taking proactive steps to prepare for worst-case scenarios can prepare you mentally and financially if an expense arises suddenly so be sure to plan and start saving today!

Credit: cnbc.com

Reduce debt

Reducing debt should be valued over accumulating savings since any payments made towards debt will result in a current benefit most likely in lower interest rates and better control over repaying later on. Paying off debts first will provide a much-needed confidence boost since living with unpaid bills introduces a great deal of stress into one's life - especially during economic downturns like the present one brought about by the Covid-19 pandemic.

In short, it can be tricky navigating financial uncertainty but having an emergency fund should always remain a priority when it comes to managing finances effectively in hard times. Taking measures such as tightening one's budget, cutting back on unnecessary spending, and strategically reducing one's debts are key steps everyone should take before confronting a large expense to mitigate further complications down the line that could cause future hardship!

Peace of mind

Being ready to handle financial emergencies can be daunting, but it's a crucial responsibility for everyone. Creating an emergency fund and taking necessary precautionary measures can offer solace, granting you financial stability and assuring confidence in dealing with exigencies. This feeling of assurance can provide a sense of safety and decrease anxiety when faced with unexpected financial pressures.

Credit: financialsamurai.com

Protecting your credit score

When it comes to financial preparedness, protecting your credit score is essential for long-term financial stability. Having a good credit score will make it more uncomplicated for you to access loans or other forms of financing should you need them. If your credit score drops too low due to negative events such as missed payments, defaulting on debt, or other causes, it could take years to rebuild your good standing with creditors and banks.

It's important to be proactive when preparing your finances in case of an emergency. Defaulting on payments can cause huge dents to your credit rating, making lenders more hesitant to trust you by providing loans with reasonable terms and interest rates. To avoid any issues, work out a plan that will help you stay on top of bills and loan payments throughout the year so that you can keep up with obligations even if an emergency arises.